People line up outside a bank branch at Dulsipur of Dang to get their social security allowance. Photo Courtesy: Live Dang.Com

People line up outside a bank branch at Dulsipur of Dang to get their social security allowance. Photo Courtesy: Live Dang.Com

About half of those who apply for bank loans become unsuccessful. Those who do receive loans are often from higher socio-economic groups.

KATHMANDU: Bank branches have been established in 752 out of the 753 local units in the country as of mid-October. There are currently 125 banks and financial institutions in the country which are operating a total of 11,632 branches.

The primary function of financial institutions is to collect deposits and disburse credit. However, national-level banks and financial institutions do not typically extend loans to low-income individuals. They only collect deposits from these groups.

About half of those who apply for bank loans become unsuccessful. Those who do receive loans are often from higher socio-economic groups. Banks, which accept deposits by opening accounts remotely in just a few minutes, have lengthy and complicated processes for granting loans to individuals, which can take months to complete.

Banker Parshuram Kunwar has pointed out that the Nepali banking sector primarily extends credit to privileged individuals and groups, while collecting deposits from disadvantaged and marginalized communities. Kunwar stated: “Banks have reached villages, but they are only mobilizing deposits and not doing anything else. Until this trend in the banking sector changes, it will not be possible for the country to achieve job creation and economic development.

A report prepared by the central bank supports Kunwar’s statement. As of the end of October, banks and financial institutions had disbursed approximately Rs 5.04 trillion in loans. Approximately 66% of this credit was extended against land plots pledged as collateral, while the remaining was disbursed against machinery, gold, motor vehicles, commercial papers, and guarantees. This indicates that access to finance is limited to those who have sufficient assets and collateral.

These findings reveal that those who are seeking to escape poverty and are in need of employment opportunities and livelihoods are still being denied access to banking services. This is despite the state recognizing financial resources as a key tool in poverty reduction.

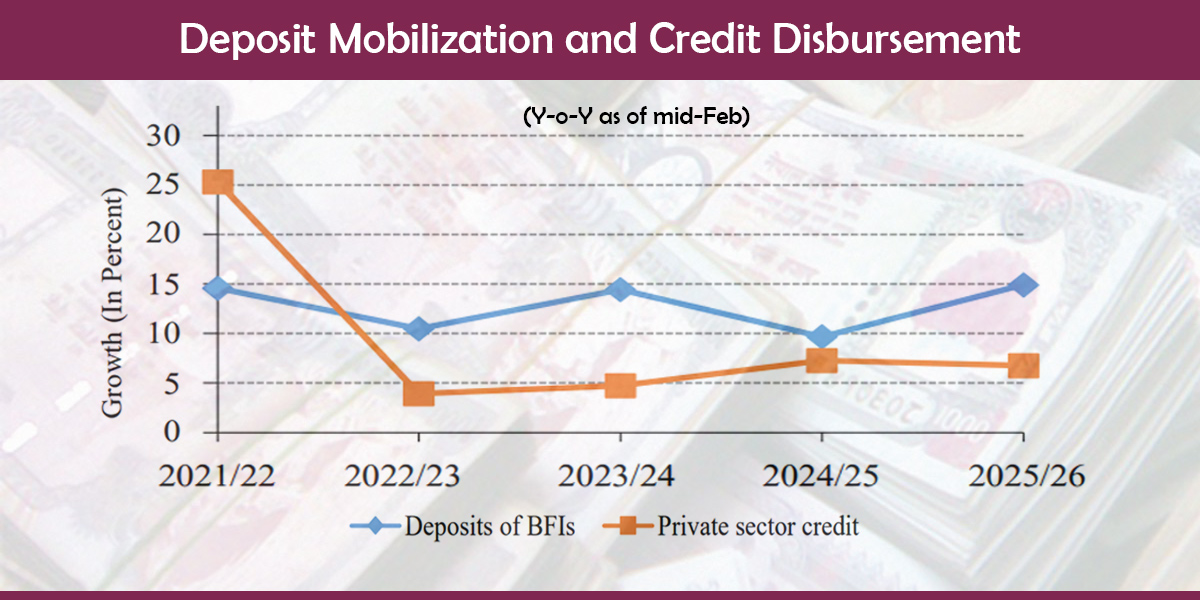

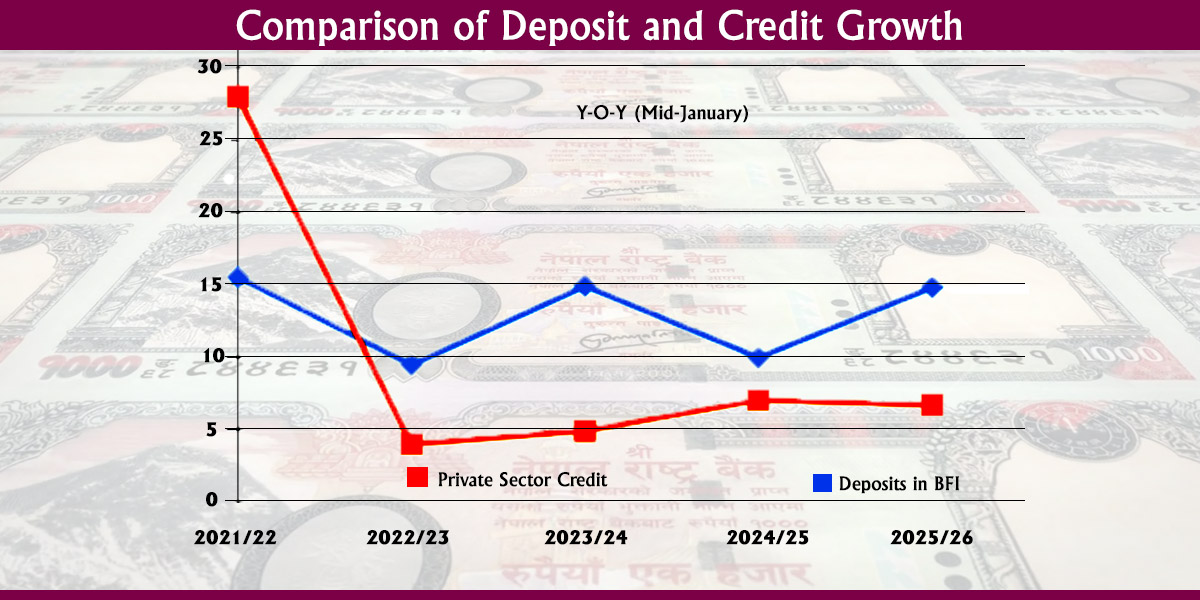

According to the central bank, as of mid-October, there are 3.63 million savings accounts in banks and financial institutions. While this number is higher than the country’s total population, banks only have 1.82 million loan accounts

According to a Baseline Survey on Financial Literacy conducted by the central bank, 71.83% of the adult population relies on moneylenders, family, and friends to meet their financial needs. This persists despite the government’s efforts to expand banking services throughout the country in order to end the need for citizens to take high-interest loans or mortgages from moneylenders.

Former Executive Director of Nepal Rastra Bank (NRB), Nar Bahadur Thapa, has commented that banks and financial institutions are making profits by collecting deposits from rural areas and investing in cities.

According to the central bank, as of mid-October, there are 3.63 million savings accounts in banks and financial institutions. While this number is higher than the country’s total population, banks only have 1.82 million loan accounts, which include multiple accounts held by the same individual or entity. This means that only about 10% of citizens have access to credit from the banking system.

There is no specific study on what percentage of total bank loans are being used by different socio-economic groups. However, experts suggest that a select few from higher socio-economic groups are using a disproportionate amount of bank loans. Thapa commented: “Only urban groups, who have the ability to mortgage property, are taking advantage of the banking system.”

Out of people’s reach

According to the Central Bureau of Statistics, Nepal’s GDP is worth approximately Rs 4.8 trillion. The total loan investment of banks is roughly the same size.

The central bank has reported that banks and financial institutions have invested Rs 519.57 billion in agricultural loans as of the end of October of the current fiscal year. This represents 12.38% of their total loans. However, many farmers in rural villages have not been able to access these loans.

In an episode of the popular Nepali social documentary series “Herne Katha”, Bishnu Bhandari, a cow farmer from Gejagaun in Syangja, shared that he was denied bank credit due to a lack of good collateral. He stated, “Banks require expensive land as collateral. Since we were denied subsidized loans with a 2% interest rate from banks, we have taken loan from a local cooperative that charges us 18% interest.”

Bhandari has called on the government to change its lending policies, arguing that genuine farmers are being denied credit while fraudulent individuals are able to access subsidized loans.

Ganesh Adhikari, who has been engaged in lime farming at Ramri in Tulsipur-1 of Dang, has also experienced difficulties in obtaining bank loans. Adhikari applied for subsidized loans at bank branches in Salyan and Dang districts, but was turned away due to a lack of land plots connected to roads. “I was seeking a loan of around Rs 3.5 million, but banks rejected my proposal. Before I could even begin my work, they asked me to show an income source to pay the installments,” he added.

As a result, Adhikari had to take a loan from a local moneylender who is charging an interest rate of 24%.

While disadvantaged groups are being denied subsidized loans, the state has provided nearly Rs 100 billion in refinancing to privileged groups in the name of COVID relief. According to the central bank, refinancing worth Rs 105.47 billion has been provided to sectors such as agriculture, micro enterprises, and exports affected by the COVID-19 epidemic as of October. The government has been providing loan subsidies under 10 headings and has allocated Rs 13.59 billion for interest subsidies in the current fiscal year alone.

In the fiscal year 2021/22, the government spent Rs 16.96 billion on interest subsidies.

The government provides subsidized loans of up to Rs 50 million for agriculture, livestock, and readymade garment projects. It also offers up to Rs 1.5 million in loans to women entrepreneurs, up to Rs 1 million in loans to foreign returnees, and up to Rs 700,000 in self-employment loans. In addition, the government provides up to Rs 1 million in business development loans to members of the Dalit community, up to Rs 500,000 in higher education and technical and vocational education loans, and up to Rs 300,000 in loans for earthquake-affected private housing construction. There are also arrangements in place to offer up to Rs 500,000 in youth self-employment loans and up to Rs 200,000 in training loans from institutions recognized by the Technical Education and Vocational Training Council.

As of mid-October, banks have provided a total of only Rs 70.01 million in youth self-employment loans, with Rs 43.6 million remaining to be disbursed.

A total of 147,642 people have taken advantage of subsidized loans, which have received a combined investment of Rs 210.47 billion from banks, as of mid-October. Out of this total, 60,061 borrowers have received Rs 138.21 billion for agriculture and livestock businesses, while 84,750 have received Rs 68.69 billion in women’s entrepreneurial loans. Banks have also invested Rs 3.57 billion in 2,831 borrowers under the remaining eight subsidized loan schemes.

Despite these investments, the grievances of the intended target group remain unchanged.

The government includes the Educated Unemployed Loan scheme in the fiscal budget with much fanfare. Under this scheme, banks are able to extend up to Rs 700,000 in loans to young people who have graduated in the current fiscal year by accepting their educational degree as collateral. However, only 145 youth have received loans under this scheme in the past five years.

As of mid-October, banks have provided a total of only Rs 70.01 million in youth self-employment loans, with Rs 43.6 million remaining to be disbursed.

Even the central bank is unaware of whether subsidized loans are being extended to the intended recipients. NRB Spokesperson Dr Gunakar Bhatta stated, “All those who complete the process are getting loans. There is no information about who is getting them and who isn’t.”

However, the central bank’s report confirms that bank credit has not reached the most disadvantaged sections of society. As of the end of October, banks and financial institutions have invested a total of Rs 245.9 billion in the energy sector, which represents 5.84% of their total investment. They have also invested Rs 98.21 billion, or 9.49% of their total lending, in MSMEs.

Private bank CEOs, however, have argued that stricter lending processes are necessary due to the central bank’s policies. One CEO of an ‘A’ class bank commented, “The central bank has implemented strict policies and we are just following them.”