Himal Press

Himal Press

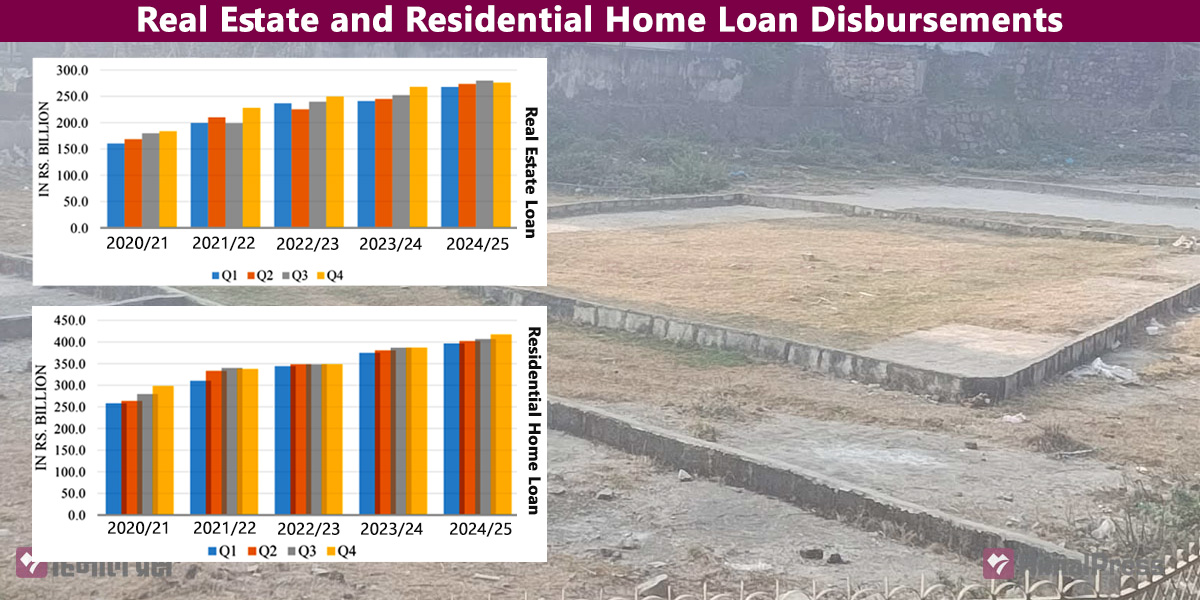

KATHMANDU: Real estate and residential home loan disbursements by banks and financial institutions (BFIs) went up by a whopping 65.83% over the past five years.

According to the Report on Status of Real Estate Transactions unveiled by the Nepal Rastra Bank (NRB) on Monday, total real estate and residential home loan disbursements increased from Rs 418.22 billion in 2020/21 to Rs 693.57 billion in 2024/25.

Disbursements of real estate loans, credit disbursed against property as collateral, increased from Rs 160.36 billion in 2020/21 to Rs 275.96 billion in 2024/25. The year-on-year (Y-o-Y) growth rate of real estate loans peaked at 24.5% in the first quarter of 2021/22, coinciding with a broader property market boom. However, growth has since moderated. Over the past four fiscal years, the average quarterly growth stood at 2.70% on a quarter-on-quarter (Q-o-Q) basis and 12.48% on a year-over-year (Y-o-Y basis.

According to the report, growth in the fourth quarter of 2024/25 fell below the multi-year average, suggesting subdued demand for real estate financing amid tighter credit conditions and a cooling property market.

In contrast, total home loan disbursements rose 1.6 times over the review period, from Rs 258.46 billion in the first quarter of 2020/21 to Rs 417.61 billion by the fourth quarter of 2024/25. Home loan volumes exceeded real estate loans in all 12 quarters covered in the study.

Growth in residential home loans has also moderated over time. Y-o-Y growth reached a high of around 26% in the second quarter of 2021/22 but averaged 10.45% over the last sixteen quarters. Q-o-Q growth averaged 2.15%.

However, the study shows no clear correlation between the growth in lending to the real estate sector, combining both real estate and residential loans, and the rise in declared property values over the same period.